30 Years Of AIM

Apparently 1995 is the 30th anniversary of AIM. There may not be that many celebrating this date, by cracking open a bottle of champagne, largely because there is absolutely nothing to celebrate. And champagne is very expensive these days. That said, those who are paid to say how wonderful it is to be listed behave as if everything is tickety-boo, and get rather miffed if anyone says anything to the contrary. However, unless you are one in ten listed companies big enough, or lucky enough in the current environment, then being private or going private is in 2025 the best thing to do. We have seen this as day after day companies de-list.

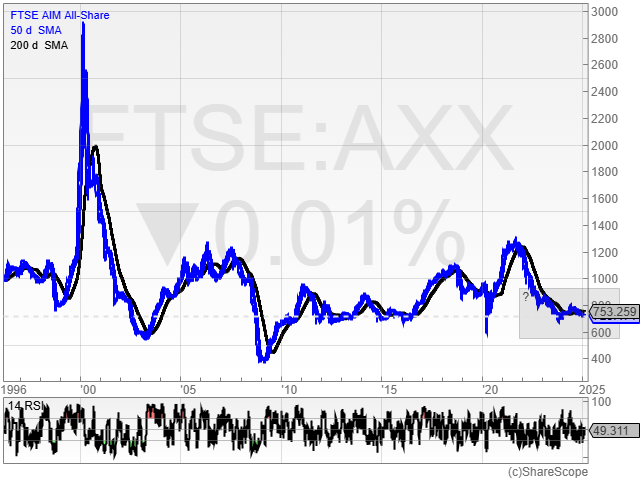

This is in fact nothing to be embarrassed about, or even a defeat of any kind, it is just common sense: it is too expensive to get / be listed, and too difficult / expensive to raise money when you get there. And of course, one is a clay pigeon for all the service providers, regulators, and psychos trying to rip off CEOs once you are in the saddle. But it does not have to be this way. Look at the contrast between the NASDAQ and AIM over the past few decades. Perhaps the real shocker here is that AIM peaked in 2000 at over 2,800, versus just under 800 25 years later.

NASDAQ

This is a complete joke, and underlines the boiled frog phenomenon that has existed on the London market year in, year out: we have a sinking feeling which has turned into a freefall. But rather than blaming economic conditions, it should be the case that the finger of blame is pointed directly at those who run the stock market. For instance, why is it half a million plus to get listed, and the same amount to remain on the stock market annually? It may be even more pricey in the USA, but as can be seen from the NASDAQ daily chart, it is worth it. Once again, I write the above, not in the expectation that anything will be done, but that things will only get worse. At the moment in the UK, the message is do not get listed, do not stay listed, as unlike Monopoly there is no £200 to collect every time you go round the board. And this was even true under the 14 years of Conservative rule, let alone with stock market / entrepreneur hating Labour. The statistic of one millionaire leaving the country every 45 minutes is not one to mess with. Even one company a week leaving AIM, it feels like it is more, is a complete disaster.

Metals One

A company which has illustrated the nature of the slings and arrows of being listed is Metals One (MET1). This week it showed how for an explorer / developer tough decisions have to be made. The main one though, is to ensure that at any given time such a company is not underfunded. Indeed, the number one error of all growth companies from Apple to Tesla to er, Premier African Minerals (PREM), is to make sure that there is enough working capital / growth capital to deliver on the strategy. Indeed, it is better to raise “too much” rather than too little, and even to dilute shareholders accordingly to ensure that a company can complete its journey successfully.

As MET1 said: “The board includes the Company’s founders and project vendors who have all been disappointed with the lack of liquidity since our IPO in 2023. This financing package secures the future of the Company’s existing projects, while allowing it to potentially diversify its exposure to a wider basket of commodities with a war chest for opportunistic acquisitions.” This was absolutely the right thing to do, especially the war chest aspect. Indeed, I would go as far to say that those who criticise the latest actions of MET1 e.g. are clearly not in touch with the realities of the stock market, both in terms of funding, and indeed, just running a PLC.

Unilever

It is so enjoyable to see a government that has in just a few months destroyed the prospects and performance of so many businesses, with so much more disaster yet to come, begging businesses and companies to come / stay in the UK, just so they can be taxed / red taped to death. The latest example of this Marxist madness is Rachel Reeves pleading with Unilever (ULVR) to spin off its Ben & Jerry’s diabetes inducing ice cream in London, rather than the admittedly second-rate Amsterdam. Unfortunately, just on the basis of trust alone, one could not recommend any company to be listed in London currently, or build a plant in Liverpool, AstraZeneca (AZN). Or do anything capital intensive. The tax and spend nightmare of government multi-decade pie in the sky projects, like the third runway at Heathrow, or the Oxbridge Silicon Valley, are all in the same vein as the failed corporatism of the 1960’s and 1970s. Funny how the benefits of the third runway idea to the UK economy was commissioned by Heathrow itself. As we know from America and latterly Ireland, it is usually the private sector, incentivised by tax breaks, that usually delivers the best results.

This Week’s Risers:

It was a good week for lithium, something which was underlined by the way that Alkemy Capital (ALK) was boosted by a tie up with utility giant Veolia. Rather more leftfield was the way that Marechale’s (MAC) investee company Weardale Lithium Limited had Durham County Council issuing a Committee Report on 28 January 2025 on Weardale’s planning application for the development of its lithium extraction project. MAC said a planning committee hearing is scheduled for 5 February 2025, and if approved, the project could become the UK’s largest lithium extraction facility. Both company’s shares have been charted on the upside well ahead of the news in the Bulletin Board Heroes charting video, with ALK from under 50p in October versus 175p now, and for MAC, earlier this month. While many still do not believe, or want to believe in the advantages of technical analysis / charting, at the very least the levels in terms of possible stop losses and targets can really help.

Model Portfolio

Indeed, I am considering starting a Model Portfolio of the best of the possible small cap situations in coming weeks. The reason for this, apart from hopefully showing that the charting works, is also to narrow down the best of the best situations, based on the setups that are the most reliable. For instance, RSI 50 rebounds, bear trap island reversals, gaps up of the bottom of the range et al.